Chapter 7 bankruptcy, often known as “liquidation bankruptcy,” allows individuals to discharge most of their unsecured debts, such as credit card debt and medical bills, by liquidating non-exempt assets. It is a viable option for those overwhelmed by debt and unable to meet their financial obligations. This form of bankruptcy is particularly beneficial for those who do not have a steady income to support a repayment plan, as it provides a relatively quick path to financial relief.

However, not all debts can be discharged under Chapter 7. Obligations such as alimony, child support, certain tax debts, and student loans typically remain after the bankruptcy process. Understanding which debts can be discharged and the implications of asset liquidation is crucial for individuals considering this option. Moreover, the process requires careful navigation of legal procedures and documentation to ensure eligibility and compliance.

How to File Chapter 7 Bankruptcy Yourself

Filing for Chapter 7 bankruptcy on your own, or “pro se,” can save money on attorney fees, but it requires a clear understanding of the legal process. The U.S. Courts provide official forms that must be filled out accurately. It’s important to research the process thoroughly, as mistakes can lead to a dismissal of your case. Additionally, individuals must be prepared to handle the administrative aspects, such as attending the meeting of creditors and managing communication with the bankruptcy trustee.

While filing pro se can be cost-effective, it’s not without challenges. Individuals must be diligent in understanding the eligibility criteria, preparing the necessary documentation, and adhering to court deadlines. Without legal guidance, the risk of errors increases, potentially jeopardizing the case. Therefore, those considering this route should evaluate their comfort level with legal procedures and their ability to manage the demands of the process independently.

How Long Does Chapter 7 Bankruptcy Take?

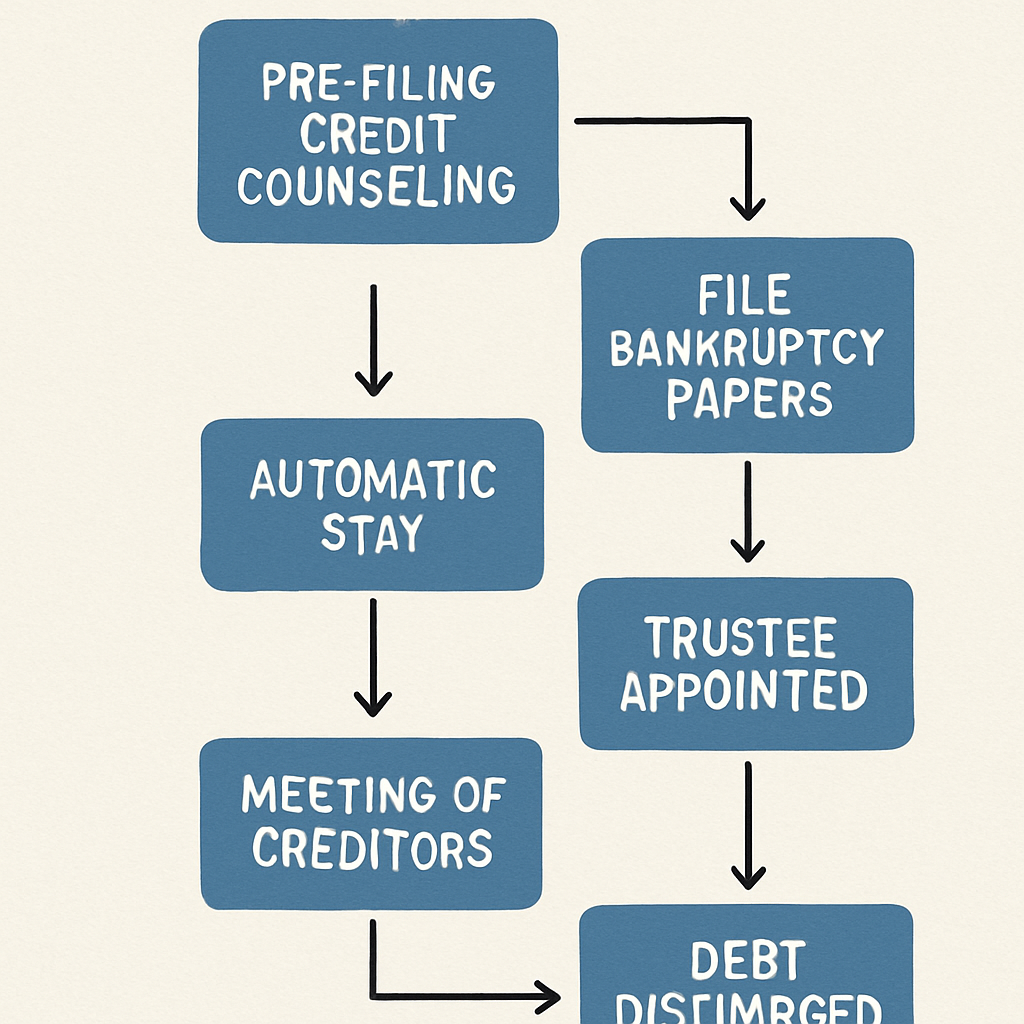

The timeline for Chapter 7 bankruptcy typically ranges from four to six months from the date of filing to the discharge of debts. However, complex cases may take longer. The process includes credit counseling, filing of documents, a meeting of creditors, and ultimately, the discharge of debts. This duration can vary based on the court’s schedule and the specifics of the debtor’s financial situation.

It’s important to note that while the process may seem lengthy, the benefits of debt discharge can provide a significant relief, allowing individuals to rebuild their financial lives. During this period, individuals must continue to meet all court requirements and provide any additional information requested by the trustee. Being proactive and organized can help streamline the process and prevent unnecessary delays.

Cost of Filing Chapter 7 Bankruptcy

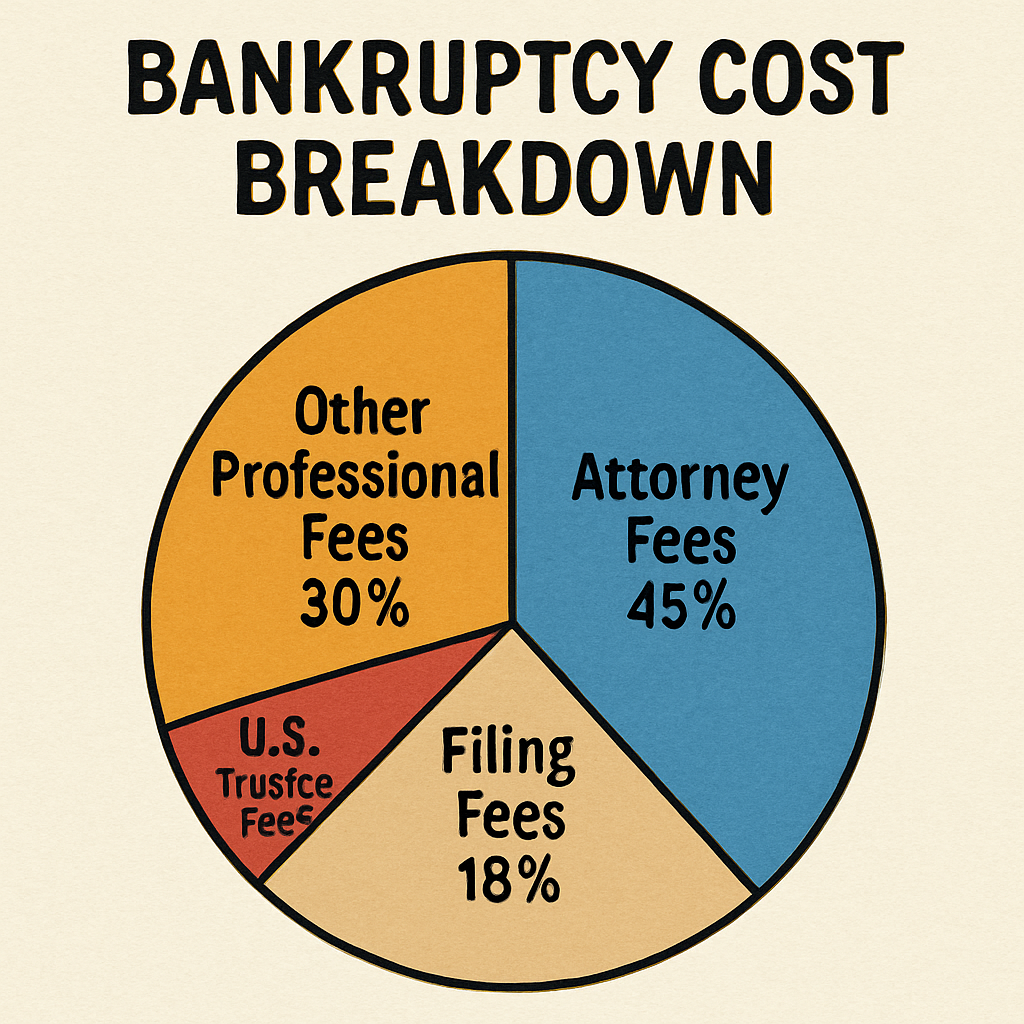

The cost of filing for Chapter 7 bankruptcy can vary based on several factors, including filing fees, attorney fees, and additional costs such as credit counseling. Understanding these costs upfront can help individuals plan financially and avoid unexpected expenses. It’s crucial to consider both mandatory fees and potential additional costs that may arise during the process.

Filing Fees for Chapter 7

The court charges a filing fee for Chapter 7 bankruptcy, which is currently $338. This fee can sometimes be paid in installments if the court approves, or waived for individuals who can demonstrate financial hardship. It’s essential for applicants to assess their financial situation and explore these options if needed, ensuring they can manage the initial costs without further strain.

In addition to the filing fee, individuals should be aware of any additional court-related expenses that may arise. These can include fees for amending filings or requesting specific documents. Being prepared for these potential costs can help individuals avoid delays in their bankruptcy proceedings.

Attorney Fees for Chapter 7

Attorney fees are often the most significant expense in a Chapter 7 bankruptcy case. The cost of hiring a bankruptcy lawyer can range from $1,000 to $3,500, depending on the complexity of the case and the attorney’s experience. While hiring a lawyer is optional, it is advisable for individuals who are unfamiliar with the legal process. A lawyer can provide guidance, ensure proper filing, and represent the individual’s interests throughout the proceedings.

Choosing the right attorney involves considering not only cost but also experience and reputation. Prospective clients should seek consultations with multiple attorneys to understand their approaches and fee structures. An experienced attorney can offer valuable insights and help navigate potential challenges, making the investment worthwhile for many individuals.

Additional Costs

- Credit Counseling: Before filing for bankruptcy, individuals must complete a credit counseling session, which typically costs between $20 and $50. This step is mandatory and ensures that applicants understand their financial situation and alternatives to bankruptcy. The session can often be completed online or over the phone, providing flexibility for participants.

- Debtor Education Course: After filing, a debtor education course is required, with costs ranging from $20 to $100. This course is designed to educate individuals on managing finances post-bankruptcy and preventing future financial difficulties. Completing this requirement is crucial for the discharge of debts, making it an essential part of the bankruptcy process.

- Miscellaneous Expenses: These can include costs for obtaining credit reports, mailing documents, and other administrative expenses. While these costs may seem minor, they can add up, so budgeting for them is important. Being organized and efficient can help minimize these expenses, allowing individuals to focus on the primary costs of the bankruptcy process.

Pros and Cons of Chapter 7 Bankruptcy

Pros

- Debt Discharge: Chapter 7 allows for the discharge of most unsecured debts, providing a fresh financial start. This relief can alleviate the stress of mounting bills and offer a clear path forward for financial recovery.

- Quick Process: Compared to other bankruptcy chapters, Chapter 7 is relatively quick. This expedited timeline can be beneficial for individuals seeking swift resolution to their financial troubles and a quicker return to financial stability.

- No Repayment Plan: Unlike Chapter 13, there is no repayment plan in Chapter 7. This means that individuals are not burdened with ongoing payments, allowing them to focus on rebuilding their finances without the pressure of a repayment schedule.

Cons

- Asset Liquidation: Non-exempt assets may be sold to pay creditors. This can lead to the loss of valuable property, which is a significant consideration for those with assets they wish to retain. Understanding exemptions and how they apply is crucial for minimizing asset loss.

- Credit Impact: Bankruptcy can significantly impact your credit score and remain on your credit report for up to 10 years. This can affect future financial opportunities, such as obtaining loans or credit cards. Individuals must weigh this long-term impact against the immediate benefits of debt discharge.

- Future Limitations: There are restrictions on filing for bankruptcy again for a certain period. This limitation means that individuals must be strategic about when to file and consider other financial planning options for future stability. It’s important to understand these restrictions and plan accordingly to avoid potential financial pitfalls.

Filing Chapter 7 Bankruptcy Online

by Martina Carinci (https://unsplash.com/@martycary)

With the advancement of technology, filing for Chapter 7 bankruptcy online has become more accessible. Several platforms offer guided assistance to help individuals complete and submit their bankruptcy forms electronically. These services can provide a structured approach, reducing the likelihood of errors in the filing process. However, it’s crucial to ensure that any online service used is reputable and compliant with legal standards.

While online filing can be convenient, individuals must remain diligent in understanding the process and verifying the credibility of the platform they choose. Reading reviews and checking for accreditation can provide assurance of a platform’s legitimacy. Additionally, some services may offer limited support, so it’s important to assess whether they meet your specific needs before proceeding.

How Many Times Can You File for Chapter 7 Bankruptcy?

The law restricts individuals from receiving a discharge under Chapter 7 if they have received a discharge in a Chapter 7 case filed within the last eight years. This rule is designed to prevent abuse of the bankruptcy system and ensure that debtors use bankruptcy as a last resort. However, there are no limits on how many times one can file for bankruptcy; only on how often you can receive a discharge.

Understanding these restrictions is vital for individuals who have previously filed for bankruptcy. It emphasizes the importance of exploring other debt relief options and financial management strategies before considering a repeat filing. Additionally, individuals should be aware of the potential implications of multiple filings on their credit history and future financial opportunities.

Can You File Chapter 7 Without a Lawyer?

Filing for Chapter 7 without a lawyer is possible, but it is not recommended for everyone. The bankruptcy process involves complex legal documentation and strict adherence to procedures. Mistakes can lead to a case dismissal or loss of property, which is why many choose to hire an experienced bankruptcy attorney. For those who opt to file pro se, a thorough understanding of bankruptcy law and meticulous attention to detail are essential.

It’s important to weigh the potential savings against the risks involved in filing without legal representation. While attorney fees can be significant, the expertise and guidance provided can often prevent costly mistakes. Individuals should assess their comfort level with handling legal matters and consider consulting with an attorney to evaluate their specific situation.

Best Chapter 7 Lawyers Near Me

Finding the right attorney can make a significant difference in the outcome of your case. It is essential to research and consult with several lawyers to find one who is experienced, reputable, and within your budget. Recommendations from friends, family, or financial advisors can be valuable in identifying potential candidates.

Evaluating an attorney’s experience with Chapter 7 cases and their approach to client communication can provide insights into their suitability for your needs. Additionally, transparency about fees and payment plans can help ensure that their services are financially feasible. Taking the time to find the right lawyer can enhance your chances of a successful bankruptcy filing.

Conclusion

Filing for Chapter 7 bankruptcy involves various fees and expenses, but it can provide significant financial relief for those burdened by debt. Understanding the costs involved, the process, and the potential outcomes can help individuals make informed decisions about their financial future. Whether choosing to file independently or with legal assistance, careful consideration and planning are key to navigating Chapter 7 bankruptcy successfully. By weighing the pros and cons and exploring all available options, individuals can embark on a path toward financial recovery and stability.

Contact TrueScope Consulting for Chapter 7 Bankruptcy support for a Rule 2004 examination or adversary proceedings.