Chapter 7 vs. Chapter 13 Bankruptcy

Navigating bankruptcy can be daunting. Understanding Chapter 7 and Chapter 13 is crucial for making informed decisions.

Chapter 7, often called “liquidation bankruptcy,” involves selling non-exempt assets to pay debts. It’s typically quicker but may require asset liquidation.

Chapter 13, known as “reorganization bankruptcy,” allows debt repayment over time while keeping assets. It’s ideal for those with steady income.

Choosing between them depends on your financial situation and goals.

This guide will help you understand the differences, benefits, and drawbacks of each option.

What Is Bankruptcy? An Overview

Bankruptcy provides a legal way to deal with overwhelming debt. It helps individuals or businesses with debt relief options.

There are different types, including Chapter 7, Chapter 11, and Chapter 13. Each serves different needs and situations.

Bankruptcy aims to offer a fresh start and fair treatment for creditors. Key features often include:

- Debt discharge or restructuring

- Legal protection from creditors

- Varied impact on assets and credit score

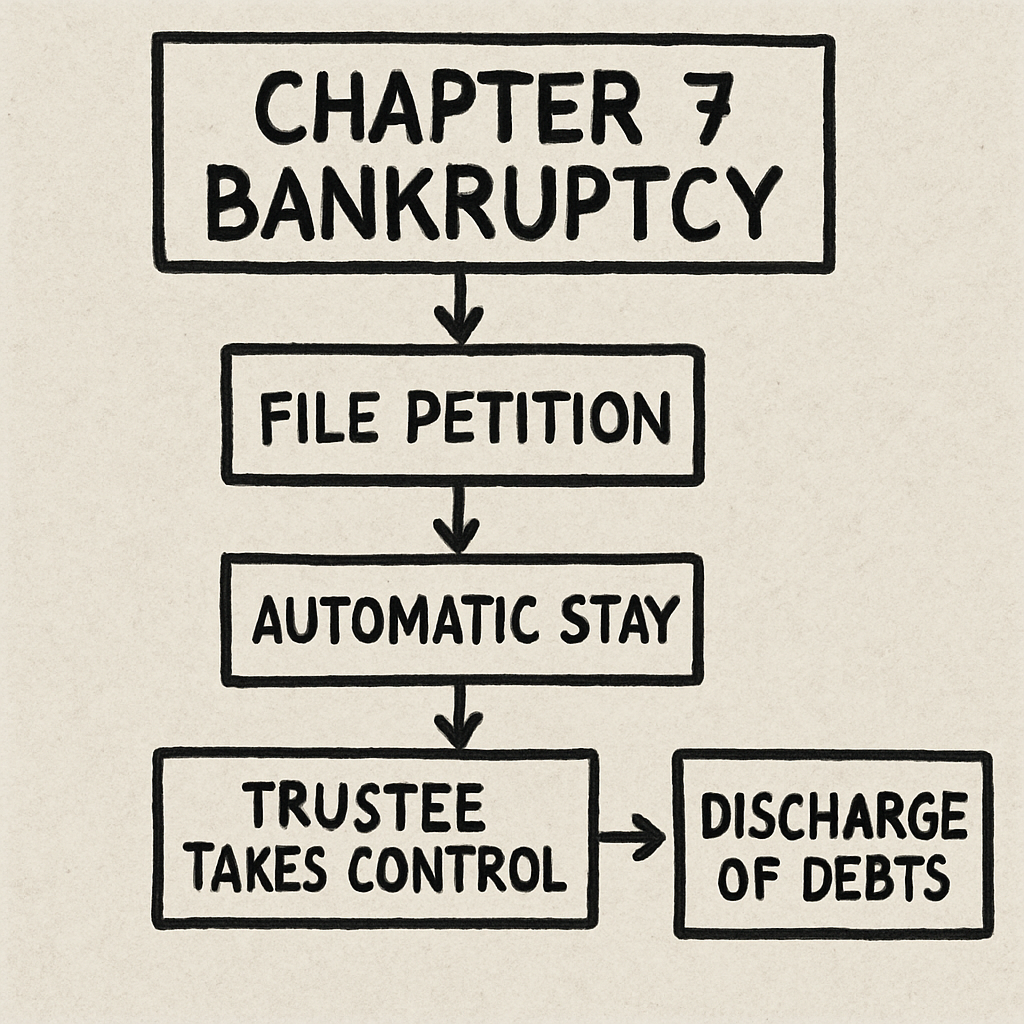

Chapter 7 Bankruptcy Explained

Chapter 7 bankruptcy is often called “liquidation bankruptcy.” It involves selling non-exempt assets to pay off creditors. This process leads to the discharge of most unsecured debts.

The entire process usually takes about 3-6 months. It’s faster than other types and provides a quick path to debt relief. However, not everyone qualifies for Chapter 7.

- Key features include:

- Liquidation of assets

- Fast debt discharge

- Strict income requirements

If eligible, debtors can eliminate overwhelming debts while keeping certain essentials. Understanding how Chapter 7 works helps determine if it’s the right choice.

Eligibility and Income Limits for Chapter 7

Eligibility for Chapter 7 relies heavily on the means test. It compares your income to your state’s median. To qualify, your income must fall below this level.

Factors considered include:

- Household size

- Monthly expenses

- Total income

The means test prevents abuse of the bankruptcy system. Those unable to pass may consider Chapter 13 instead.

What Happens to Your Assets in Chapter 7?

In Chapter 7, non-exempt assets are liquidated. This process helps repay creditors. However, certain essential items are protected.

Common exempt assets include:

- Primary home equity (up to a limit)

- Basic furnishings

- Necessary clothing

State and federal laws determine asset exemptions. Consulting with an attorney ensures correct asset protection.

How Long Does Chapter 7 Last and What Does It Cost?

Chapter 7 typically wraps up in three to six months. Its brevity makes it appealing to many debtors. The cost involves court and attorney fees.

- Typical costs include:

- Court filing fees

- Attorney fees

Costs vary by location. It’s crucial to understand the financial commitment involved.

Pros and Cons of Chapter 7 Bankruptcy

Chapter 7 offers significant benefits. However, it has downsides too. Weighing pros against cons aids decision-making.

Advantages:

- Quick debt relief

- Discharge of most debts

Disadvantages:

- Asset liquidation risk

- Impact on credit score

Knowing both pros and cons aids in making informed financial choices.

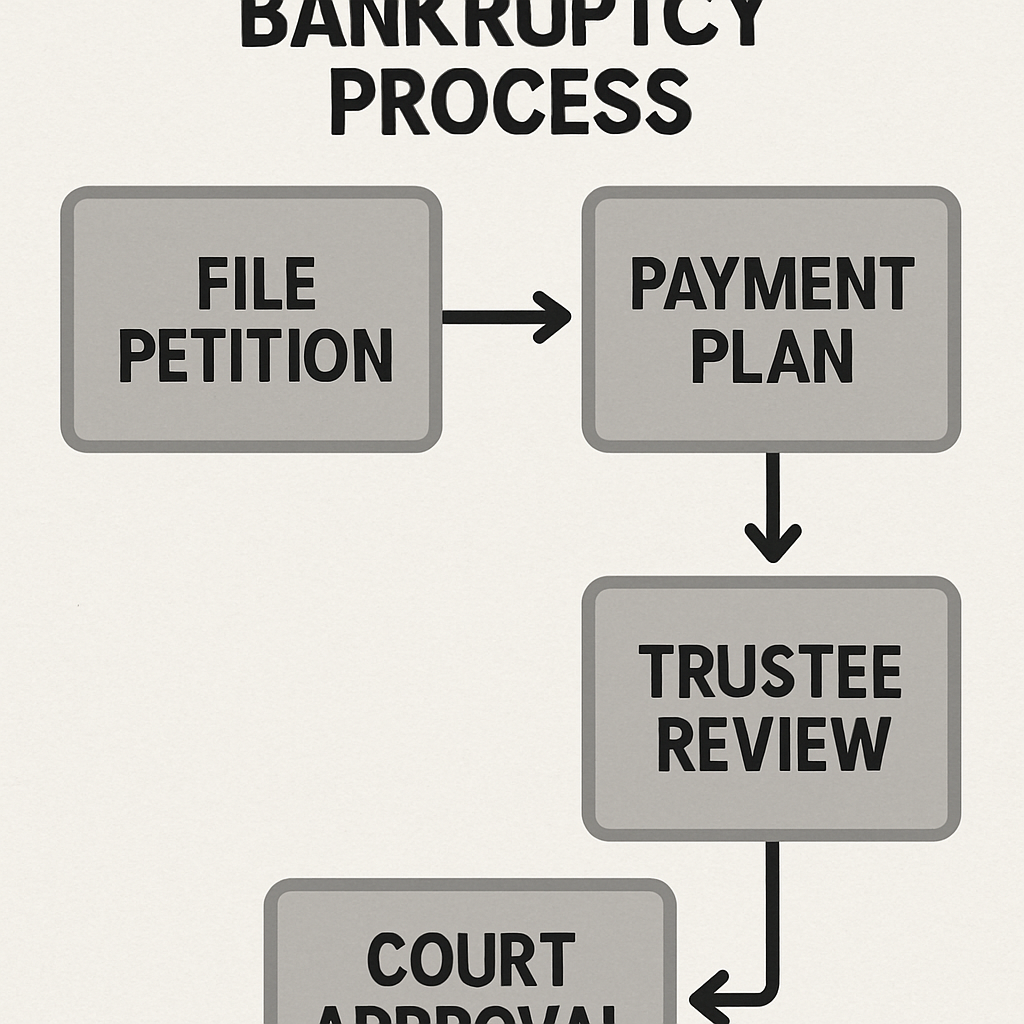

Chapter 13 Bankruptcy Explained

Chapter 13 bankruptcy is known as “reorganization bankruptcy.” It enables individuals to keep their assets while repaying debts. This repayment is structured over a 3-5 year period.

Debtors propose a repayment plan for court approval. It prioritizes secured debts and arrears first. Meanwhile, unsecured debts are paid based on disposable income.

Key features include:

- Asset retention

- Court-approved repayment plan

- Debt consolidation

This option suits those with regular income wanting to maintain their property. Understanding Chapter 13 helps individuals manage debt effectively.

Who Qualifies for Chapter 13?

To qualify for Chapter 13, individuals need steady income. This ensures they can meet repayment obligations. Debt limits are also in place for eligibility.

Considerations include:

- Stable monthly income

- Debt limits

- Detailed payment plan

Meeting these criteria is essential for court approval. Debtors must demonstrate their ability to complete payments.

How Chapter 13 Repayment Plans Work

Chapter 13 plans restructure debts into manageable payments. Court approval requires detailed budgeting. Payments consolidate existing debts into one monthly installment.

Essential plan elements include:

- Three to five-year timeline

- Priority debt repayment

- Adjusted living expenses

The repayment plan affords debtors fresh financial starts. It also protects valuable assets from immediate liquidation.

Pros and Cons of Chapter 13 Bankruptcy

Chapter 13 offers unique benefits but has drawbacks too. These considerations affect decision-making.

Advantages:

- Keeps assets intact

- Protects from foreclosure

Disadvantages:

- Longer duration

- More expensive than Chapter 7

Balancing these factors with personal goals helps choose an appropriate bankruptcy path.

Chapter 7 vs Chapter 13 Bankruptcy: Key Differences

The differences between Chapter 7 and Chapter 13 bankruptcy are crucial. They impact financial stability and asset retention.

Chapter 7 Highlights:

- Quick debt discharge

- Possible asset liquidation

- Short duration

Chapter 13 Highlights:

- Asset protection

- Structured repayment plan

- Longer timeframe

Eligibility plays a significant role too. Chapter 7 requires passing the means test. Meanwhile, Chapter 13 demands a steady income for repayments.

Choosing between these options depends on individual circumstances. Assess income, assets, and debt types carefully.

Ultimately, understanding these distinctions aids in making informed financial decisions.

Which Is Better: Chapter 7 or Chapter 13?

Determining whether Chapter 7 or Chapter 13 is better depends on personal financial goals. Each option offers distinct advantages and considerations.

Chapter 7 may suit those with limited income and minimal assets to protect. It’s ideal for quick debt relief.

Chapter 13 benefits individuals with regular income seeking to retain valuable assets. It allows for debt management through structured repayment.

Considerations:

- Income stability

- Asset retention needs

- Debt repayment capacity

Ultimately, the best choice aligns with your financial priorities and objectives.

Special Considerations and Common Questions

When considering bankruptcy, specific questions arise frequently. Can you retain essential assets? Are there limitations on future filings?

Common Queries:

- What assets are exempt?

- How does bankruptcy impact credit?

- Are retirement savings protected?

Understanding these nuances helps guide decision-making. It’s vital to consult legal advice for personalized solutions.

Additional Considerations:

- Impact on co-borrowers

- Tax implications

- How automatic stays affect creditors

Research and expert consultation ensure compliance with all legal requirements. Tailored advice considers individual circumstances.

Can I Keep My House or Car?

Many worry about losing their homes or vehicles. Chapter 13 often allows retention if conditions are met. Chapter 7 may offer exemptions under specific criteria.

Possible Options:

- Current on payments

- Equity within exemption limits

How Often Can You File Bankruptcy?

Bankruptcy filings are subject to time restrictions. You can file Chapter 7 every eight years. Chapter 13 has shorter intervals.

Filing Intervals:

- Chapter 7: every 8 years

- Chapter 13: every 2 years

Can I File Chapter 13 After Chapter 7 (or Vice Versa)?

Switching from one bankruptcy type to another involves specific rules. Filing Chapter 13 after Chapter 7 is possible, but restrictions apply.

Key Points:

- Waiting periods exist

- Legal requirements must be met

Chapter 7 vs Chapter 13 vs Chapter 11: A Brief Comparison

Understanding the differences among Chapter 7, 13, and 11 is crucial for making informed financial decisions. Each type serves different purposes and eligibility criteria.

Comparison Highlights:

- Chapter 7: Personal liquidation, quick discharge.

- Chapter 13: Personal reorganization, extended payment plan.

- Chapter 11: Business reorganization, more complex procedure.

Choosing the right chapter depends on the individual’s or business’s specific needs and financial situation. Consulting a legal expert can clarify the best path forward.

Steps to Filing Bankruptcy and What to Expect

Filing bankruptcy requires careful preparation and understanding of the legal process. It can be a path to financial relief but comes with responsibilities.

Here is a general outline of the steps:

- Complete credit counseling.

- File paperwork with the court.

- Attend a creditors’ meeting.

- Complete debtor education.

Throughout the bankruptcy process, expect close scrutiny of your financial details. Working with an attorney is often recommended to ensure compliance and protection of your rights.

When to Consult a Bankruptcy Attorney

Determining when to consult a bankruptcy attorney can be crucial. Legal advice can provide clarity and guide your decisions.

Reasons to consult an attorney include:

- Complex financial situations.

- Uncertainty about eligibility.

- Advice on asset protection.

Consulting a knowledgeable attorney can help you navigate the process with confidence. They can assist you in evaluating options and making informed choices.

Conclusion: Making the Right Choice for Your Financial Future

Choosing between Chapter 7 and Chapter 13 is a pivotal financial decision. Consider your assets, debts, and future goals.

A thoughtful evaluation of your financial situation, coupled with expert advice, can lead you to the best bankruptcy option.

Contact TrueScope Consulting for Chapter 7 adversary proceeding auditor services or for Chapter 11 monthly operating report related services.