Navigating the complex world of bankruptcy can be daunting, especially when it involves understanding the implications of a dismissed Chapter 13 bankruptcy case. Filing for Chapter 13 bankruptcy often presents a viable option for individuals seeking a structured path to financial relief. It offers a strategic approach to reorganizing debt and establishing a manageable repayment plan over a specified period. However, not all cases proceed smoothly to completion; some are dismissed, leaving filers uncertain about the repercussions and their next steps.

This article aims to demystify the circumstances leading to a Chapter 13 dismissal, explore its impact on your financial landscape, and outline potential actions if you find yourself in this situation. Knowing the ins and outs of bankruptcy dismissal can equip you with the knowledge to navigate these financial waters more effectively.

Before delving into the specifics of Chapter 13 dismissals, it’s essential to clarify what a bankruptcy dismissal entails in general terms. When a bankruptcy case is dismissed, the court effectively ends the proceedings without discharging the debtor’s obligations. This means that the legal protections you sought against creditors are lifted, and your financial situation reverts to its pre-filing status, minus any fees or payments made during the process.

This reversal can be a significant setback, as it reinstates the stress and pressure of unpaid debts. Understanding this concept is vital as it underscores the importance of adhering to the court’s requirements and the terms of your bankruptcy plan. A dismissal indicates an incomplete resolution of your financial issues, which can have lasting effects on your fiscal health and creditworthiness.

Chapter 13 bankruptcy, often known as a “wage earner’s plan,” allows individuals with regular income to craft a repayment strategy to address all or a portion of their debts. Unlike Chapter 7 bankruptcy, which involves liquidating assets to repay creditors, Chapter 13 focuses on income-based repayment plans. These plans typically span three to five years, offering a structured timeline for debt settlement.

This form of bankruptcy provides a unique opportunity for debtors to retain their assets while systematically repaying creditors under court supervision. The repayment plan is tailored to the individual’s financial capacity, ensuring that payments are feasible and sustainable over the long term. As such, Chapter 13 is often viewed as a more constructive approach to managing debt, allowing individuals to maintain their financial stability while addressing their obligations.

Common Reasons for Dismissing Chapter 13 Bankruptcy

Understanding why a Chapter 13 case might be dismissed is crucial for avoiding this outcome. Here are some common reasons:

- Failure to Make Payments: The most frequent cause of dismissal is the debtor’s inability to adhere to the agreed payment plan. Consistently missing payments or making late payments can lead to dismissal. This underscores the importance of a realistic and achievable repayment plan that aligns with your financial capabilities.

- Incomplete Paperwork: Filing for bankruptcy involves a significant amount of paperwork. If documents are missing or incomplete, the court may dismiss the case. Ensuring that all required documentation is accurate and submitted on time is critical to avoiding procedural dismissals.

- Non-compliance with Court Orders: Failing to comply with court orders or attend mandatory meetings, such as the 341 meeting of creditors, can result in dismissal. Compliance is key to maintaining the court’s trust and the protective status of your bankruptcy case.

- Fraud or Misrepresentation: Any attempt to deceive the court by hiding assets or providing false information can lead to a case being dismissed. Transparency and honesty are fundamental to a successful bankruptcy filing, as any misrepresentation can have severe legal repercussions.

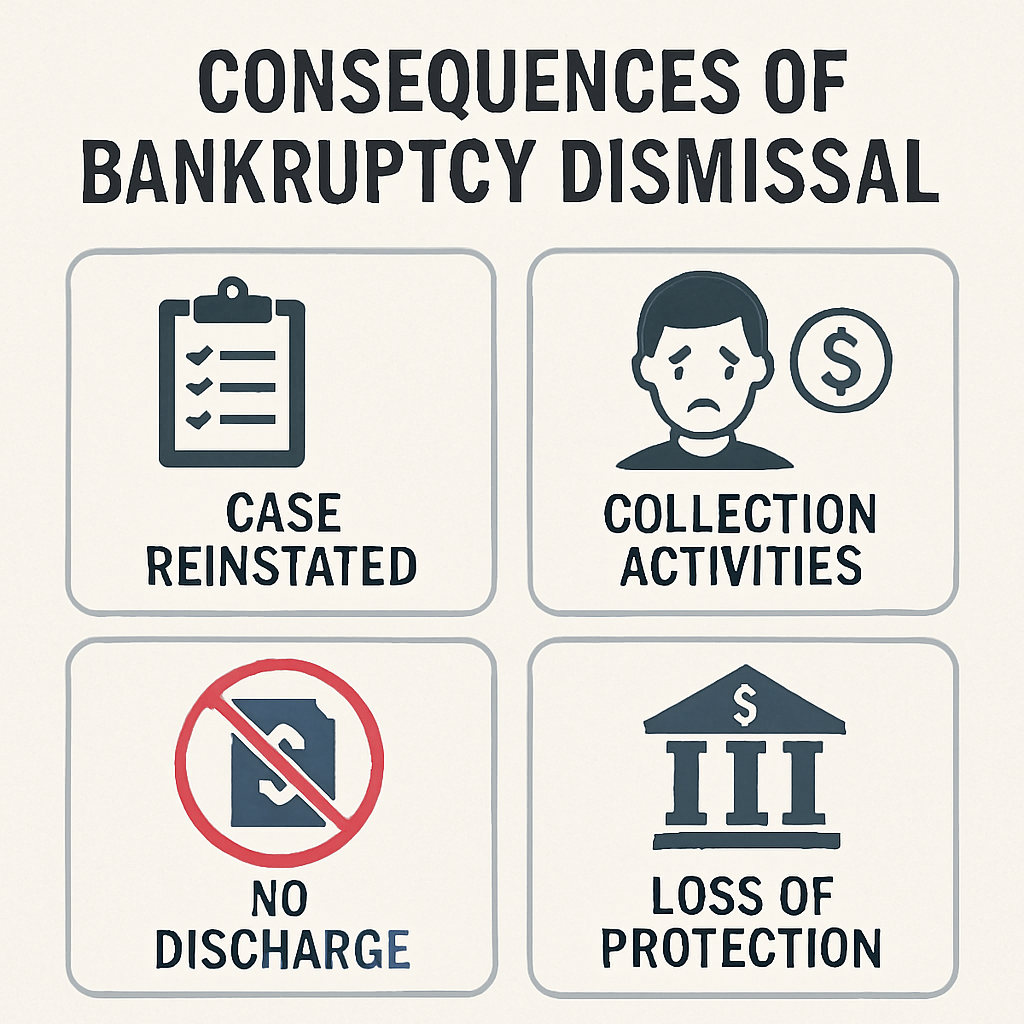

Consequences of a Dismissed Bankruptcy

When a Chapter 13 bankruptcy is dismissed, the consequences can be significant:

- Loss of Automatic Stay: The automatic stay that protected you from creditor actions is lifted. Creditors can resume collection efforts, including lawsuits, wage garnishments, and foreclosures. This sudden exposure can reignite financial pressures and jeopardize any progress made during the bankruptcy period.

- Impact on Credit Score: Although filing for bankruptcy already affects your credit score, a dismissal can exacerbate this impact. It indicates an inability to complete the bankruptcy process, which can be perceived negatively by potential lenders and creditors. This can hinder future financial endeavors, such as securing loans or credit.

- Loss of Payments Made: Payments made during the bankruptcy process are not returned. If your plan was dismissed, you will not receive a refund for payments made to the trustee. This loss can be financially burdensome, especially if significant amounts were paid towards reducing your debt.

- Legal and Trustee Fees: Any legal or trustee fees paid during the process are typically non-refundable. These fees, often substantial, are an additional financial burden that remains even after the case is dismissed.

What to Do If Your Chapter 13 Case Is Dismissed

If your Chapter 13 bankruptcy case is dismissed, there are several steps you can take:

Refile for Bankruptcy

One option is to refile for bankruptcy. However, this path may not be straightforward. If your case was dismissed due to non-compliance or failure to follow the court’s rules, you may face a waiting period before refiling. It’s essential to address the issues that led to the initial dismissal to increase your chances of success in a subsequent filing.

Refiling requires careful consideration of your financial situation and the reasons behind the previous dismissal. Consulting with a legal professional can provide guidance on whether refiling is a viable option and how to approach it effectively.

Modify Your Repayment Plan

In some cases, it may be possible to modify your repayment plan to better align with your financial situation. Adjusting the plan to reflect changes in income or expenses can sometimes prevent dismissal or enable you to refile successfully. This flexibility is a critical component of Chapter 13 bankruptcy, allowing for adjustments that accommodate unforeseen financial challenges.

Working with a bankruptcy attorney can help you negotiate modifications with the court, ensuring that your repayment plan remains feasible and compliant with legal requirements. This proactive approach can safeguard your bankruptcy case from future dismissals.

Seek Legal Advice

Consulting with a bankruptcy attorney can provide clarity on your specific situation. They can help you understand your options, whether it’s refiling, modifying your plan, or exploring alternative debt solutions. A legal expert can offer insights into the complexities of bankruptcy law, helping you make informed decisions tailored to your circumstances.

Legal advice can also provide peace of mind, knowing that you have a professional advocate navigating the intricacies of bankruptcy proceedings on your behalf. This support can be invaluable in charting a course towards financial recovery.

Preventing a Dismissal: Best Practices

To avoid the pitfalls of a dismissed Chapter 13 bankruptcy, consider these best practices:

- Stay Current with Payments: Ensure that you make all scheduled payments on time. Setting up automatic payments can help avoid missed deadlines. Consistent payment adherence is crucial in maintaining the court’s trust and the protective benefits of your bankruptcy status.

- Accurate Paperwork: Double-check that all paperwork is complete and accurate before submission. Working with a qualified attorney can ensure that you meet all filing requirements. Meticulous attention to detail can prevent procedural dismissals and demonstrate your commitment to resolving your debts.

- Attend Required Meetings: Make sure to attend all required meetings and hearings, such as the 341 meeting of creditors. These meetings are integral to the bankruptcy process, providing an opportunity to demonstrate compliance and transparency to the court and your creditors.

- Open Communication: Maintain open communication with your trustee and attorney. If you foresee any issues with your payment plan, discuss them promptly. Proactive communication can address potential challenges before they escalate, keeping your bankruptcy case on track.

Conclusion

Filing for Chapter 13 bankruptcy can be a lifeline for those struggling with debt, offering a structured way to regain financial stability. However, understanding the reasons for dismissal and taking proactive measures can help ensure a successful outcome. By staying informed and diligent throughout the process, you can navigate the complexities of bankruptcy more effectively and avoid the setbacks of a dismissed case.

Remember, seeking professional guidance is always a wise step to ensure you’re on the right track. With the right support and strategies, you can overcome financial challenges and work towards a more secure future.